Understanding Defective Grantor Trusts: Leveraging Tax Rules to Transfer Wealth Efficiently

How Intentionally Defective Grantor Trusts Help Move Appreciating Assets Outside the Estate

Sophisticated estate planning often involves structuring trusts that take advantage of the way different tax rules interact. One of the most powerful examples is the Defective Grantor Trust, commonly known as an Intentionally Defective Grantor Trust (IDGT). Despite its unusual name, the trust is not defective in a practical sense. The “defect” refers to a deliberate tax feature that allows the trust to be treated differently for income tax purposes than for estate and gift tax purposes.

This unique treatment can create significant planning advantages. Assets transferred into the trust are removed from the grantor’s taxable estate, while the grantor continues to pay the income taxes generated by those assets. Over time, this allows the trust to grow more efficiently for future beneficiaries while simultaneously reducing the taxable estate of the grantor.

Defective Grantor Trusts are widely used in long-term wealth transfer strategies, particularly when clients hold assets expected to appreciate substantially in value.

What Is a Defective Grantor Trust?

A Defective Grantor Trust is an irrevocable trust that is intentionally structured so that the grantor remains responsible for paying income taxes on trust earnings, even though the trust assets are no longer included in the grantor’s estate for estate tax purposes. (commercetrustcompany.com)

The structure works by drafting the trust with specific provisions that cause the IRS to treat the grantor as the “owner” of the trust for income tax purposes while recognizing the transfer as complete for estate and gift tax purposes. This dual tax treatment is what makes the strategy so effective.

Assets are typically transferred to the trust either through a gift, a sale to the trust, or a combination of both. Because the trust is irrevocable, the transferred assets and any future appreciation are removed from the grantor’s estate.

Core Features of a Defective Grantor Trust

- Irrevocable trust designed to move assets outside the grantor’s taxable estate

- Grantor remains responsible for income taxes on trust earnings

- Assets may be transferred through gifts, sales, or hybrid strategies

- Future appreciation of assets occurs outside the grantor’s estate

- Often used with high-growth assets such as businesses, real estate, or concentrated stock positions

- Beneficiaries are typically children or future generations

Why Defective Grantor Trusts Are Used

The core objective of a Defective Grantor Trust is to shift appreciating assets out of an estate while allowing the trust assets to grow without being reduced by income taxes. Because the grantor pays the tax liability personally, the trust’s assets remain intact and can compound more efficiently over time.

From a planning perspective, this structure can create a powerful wealth transfer effect. The grantor’s estate is gradually reduced by the income taxes they pay on behalf of the trust, while the trust itself grows free of that tax burden. In addition, many strategies involve selling appreciating assets to the trust in exchange for a promissory note, effectively “freezing” the value of the grantor’s estate at the time of the transaction. (Fidelity)

This makes Defective Grantor Trusts particularly attractive for individuals holding assets expected to increase substantially in value over time.

Common Use Cases

- Business owners transferring equity to future generations

- Families seeking to move appreciating assets outside the taxable estate

- Clients with concentrated stock positions expected to grow

- Estate planning strategies that combine gifts and installment sales

- Multigenerational planning involving long-term wealth preservation

Advantages of the Defective Grantor Trust Structure

The effectiveness of the Defective Grantor Trust lies in its unique tax treatment. Because the grantor remains responsible for the income tax obligations of the trust, the trust assets are able to grow without being reduced by taxes. This increases the amount of wealth ultimately transferred to beneficiaries.

At the same time, the payment of those taxes further reduces the grantor’s estate without being treated as an additional taxable gift. This combination allows the trust to serve as a highly efficient wealth transfer vehicle.

When implemented as part of a broader estate plan, the strategy can also be combined with generation-skipping planning, family governance structures, and long-term trust administration.

Key Benefits

- Removes appreciating assets from the grantor’s taxable estate

- Allows trust assets to grow without income tax erosion

- Reduces the grantor’s estate through tax payments over time

- Supports long-term wealth transfer to future generations

- Flexible planning opportunities through gifts or asset sales to the trust

Risks and Structural Considerations

While Defective Grantor Trusts can provide substantial planning benefits, they must be carefully structured and administered. The trust must contain specific provisions that trigger grantor trust status for income tax purposes without causing the trust assets to be included in the grantor’s estate.

In addition, the grantor must be financially able to pay the ongoing income taxes generated by the trust assets. Although this tax burden is often considered a strategic advantage, it still represents a real obligation that must be accounted for in the planning process.

Another important consideration is that assets held in the trust generally do not receive a step-up in basis at the grantor’s death because they are not included in the taxable estate.

Key Considerations

- Trust must be properly drafted to achieve grantor trust tax treatment

- Grantor must be able to pay the ongoing income tax obligations

- Assets transferred to the trust are generally not eligible for a step-up in basis

- Estate planning and tax professionals must coordinate closely when structuring the trust

- Ongoing administration and compliance are essential

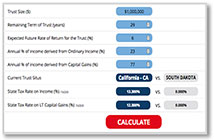

The Role of Jurisdiction in Trust Planning

The legal environment in which a trust is established can have a meaningful impact on its effectiveness. States with modern trust statutes provide greater flexibility, stronger asset protection, and improved long-term planning opportunities.

South Dakota has emerged as one of the most favorable trust jurisdictions in the United States due to its advanced trust laws, strong privacy protections, and absence of state income tax on trust assets. (Sterling Trustees)

For complex structures such as Defective Grantor Trusts, these advantages can enhance the long-term stability and effectiveness of the overall planning strategy.

Summary: Defective Grantor Trusts at a Glance

| Feature | Details |

| Trust Type | Irrevocable grantor trust |

| Tax Treatment | Outside the estate for estate tax purposes but taxed to the grantor for income tax |

| Primary Objective | Transfer appreciating assets outside the estate |

| Income Tax Responsibility | Paid by the grantor |

| Ideal Use | High-growth assets and long-term wealth transfer strategies |

Learn More

Sterling Trustees works with advisors, attorneys, and families to administer sophisticated trust structures designed to support long-term wealth preservation. As an independent South Dakota trust company focused exclusively on trust administration, we collaborate closely with advisory teams to implement and manage complex trusts with precision and transparency.

To learn more about Defective Grantor Trusts and other planning strategies, email us or visit sterlingtrustees.com

Download this article

Let’s talk. Schedule a date and time to talk about the benefits to your practice of working with an independent corporate trustee.