Understanding SLATs: A Strategic Tool for Wealth Preservation

Why Spousal Lifetime Access Trusts Continue to Play a Critical Role in Modern Estate Planning

For individuals and families focused on long-term wealth preservation, the Spousal Lifetime Access Trust (SLAT) offers a compelling mix of estate tax efficiency, asset protection, and flexibility. This irrevocable trust structure allows one spouse to transfer significant assets out of their taxable estate while preserving indirect access to those assets through the other spouse. As exemption levels and tax laws continue to shift, the SLAT remains a highly strategic option in many estate planning conversations.

SLATs are increasingly relevant for those who want to take advantage of current estate planning opportunities without fully relinquishing the practical benefits of the assets they intend to transfer. Understanding how SLATs are structured, when to use them, and what their benefits and limitations are can help financial and legal professionals guide clients toward well-informed, forward-looking decisions.

What Is a SLAT Trust?

A Spousal Lifetime Access Trust is an irrevocable trust created by one spouse (the donor) for the benefit of the other spouse (the non-donor), and potentially other beneficiaries such as children or grandchildren. The donor contributes individually owned assets to the trust, using their lifetime gift tax exemption to remove the assets from their taxable estate. The trust can be structured to ensure that the donor spouse’s gift is excluded from both their own estate and that of the non-donor spouse.

Although the donor spouse gives up legal ownership and direct access to the assets, they may still benefit indirectly through the non-donor spouse, who can receive distributions of income and principal during their lifetime. The SLAT is usually treated as a grantor trust for income tax purposes, meaning the donor pays the income taxes on any income generated by the trust. This payment is not considered a gift and further reduces the donor’s taxable estate without additional transfer taxes.

Core Features of a SLAT:

- Created by one spouse for the benefit of the other and future generations

- Funded with individually owned assets, not jointly held property

- Removes assets from the taxable estate of both spouses if structured properly

- Non-donor spouse may access income and principal

- Donor spouse pays income taxes, allowing the trust to grow tax-free

- GST exemption can be allocated for multigenerational planning

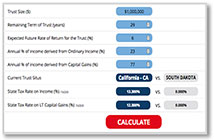

The Role of Jurisdiction: Why South Dakota Matters

Where a trust is established can have a major impact on its performance, flexibility, and legal protections. South Dakota continues to be recognized as one of the most advantageous jurisdictions for modern trust structures. The state’s statutes allow for trusts of unlimited duration, offer powerful asset protection laws, and permit enhanced privacy features, including the ability to seal trust documents in court proceedings.

Sterling Trustees is chartered in South Dakota and specializes in working with advisors and estate planners to administer complex trusts like SLATs in a way that fully leverages the state’s legal framework. For clients concerned about creditor protection, multigenerational planning, and tax neutrality, South Dakota offers a superior legal environment.

Why Clients Use SLATs

SLATs are often used in cases where a client is seeking to reduce their taxable estate while maintaining some level of access to the assets they are transferring. By establishing a SLAT, clients can take advantage of current gift and estate tax exemptions while keeping wealth within reach through their spouse. The ability to make a large gift, enjoy potential asset protection benefits, and still maintain some financial flexibility is what makes SLATs so valuable.

The structure is especially appealing to married couples who want to begin multigenerational planning but are not ready to give up full control or utility of the assets involved. In addition, SLATs can be customized to include specific terms for distributions, beneficiary classes, and trustee appointments, giving clients and their advisors additional control over how the trust is administered.

Common Use Cases:

- Couples concerned about future reductions in estate tax exemptions

- Clients with fast-appreciating assets who want to move them out of their estate now

- Families seeking long-term, multigenerational planning structures

- Individuals wanting to make a large gift while preserving liquidity options

- Clients with creditor protection or divorce concerns

Advantages of the SLAT Structure

The SLAT’s unique strength lies in its ability to deliver estate tax benefits while maintaining a measure of practical flexibility. Because the donor spouse pays the taxes on trust income, the trust assets are allowed to grow without erosion. This can result in significant wealth accumulation over time.

A properly structured SLAT can also help shield assets from creditors, protect family wealth in the event of a divorce, and provide a reliable vehicle for future charitable or generational giving. When the trust is established in a jurisdiction like South Dakota, those benefits are amplified through favorable laws governing asset protection, trust duration, and privacy.

Key Benefits:

- Removes assets from both spouses’ estates, reducing potential estate tax exposure

- Offers indirect access to wealth through the non-donor spouse

- Allows tax-free growth of trust assets through grantor trust taxation

- Supports legacy and GST planning across generations

- Can be structured to offer strong protection from creditors or divorcing spouses

Risks and Structural Considerations

Despite its many benefits, the SLAT must be carefully drafted and implemented. As an irrevocable trust, the terms generally cannot be changed once the assets are contributed. Advisors must also account for scenarios that could alter the intended benefits of the structure, such as divorce or the premature death of the non-donor spouse, which could eliminate the donor’s indirect access to trust assets.

SLATs also do not provide a step-up in basis at death, which can have long-term implications for capital gains taxes. Additionally, to avoid estate inclusion, it is critical that all contributed assets are individually owned by the donor spouse—not held jointly at the time of transfer. A poorly drafted or executed SLAT may unintentionally include trust assets in one or both spouses’ estates or result in unfavorable tax treatment.

Key Considerations:

- Trust is irrevocable; terms cannot be changed once funded

- Divorce or death of the non-donor spouse can eliminate indirect access

- Assets do not receive a step-up in basis at death

- Proper ownership and separation of assets is critical before funding

- Must meet technical requirements to avoid inclusion in either estate

When a SLAT Is Worth Considering

The Spousal Lifetime Access Trust offers a unique opportunity to reduce estate taxes, protect family wealth, and preserve access to assets under the right conditions. It is not the right tool for every client, but for those with significant wealth, strong spousal trust, and a desire to engage in forward-looking estate planning, it can be a cornerstone of a well-structured strategy.

As always, successful implementation depends on experienced legal counsel, thoughtful collaboration among advisors, and proper trust administration. With careful planning, a SLAT can help clients take control of their estate tax exposure while building a long-term framework for legacy preservation.

Learn More

Sterling Trustees is an independent, South Dakota-chartered trust company focused exclusively on trust administration. We do not manage investments or sell financial products. Our work is conflict-free and designed to support the advisory teams our clients rely on.

To explore how we help structure and administer SLATs and other advanced trusts, contact us or read more here.

Download this article

Let’s talk. Schedule a date and time to talk about the benefits to your practice of working with an independent corporate trustee.