Navigating Trust Structures: Directed vs. Discretionary Trusts

In the intricate landscape of wealth management and asset protection, the selection of a trust structure is a pivotal decision that profoundly influences the preservation and growth of assets for generations. Today, we delve deeper into directed and discretionary trusts, deciphering their nuances and implications.

Directed Trusts: Steering Trust Management with Precision

In a directed trust, the trustee’s role is narrowly defined to administrative tasks, asset safeguarding, and executing explicit directives outlined by a designated investment or distribution advisor or committee. This advisor assumes a central role in directing crucial decisions such as investment strategies, asset allocation, and distributions as per the trust’s terms.

For instance, imagine a family establishes a trust where the trustee is responsible for managing administrative functions and ensuring compliance with legal obligations. Concurrently, an investment advisor or committee, comprising financial experts or trusted advisors, guides investment decisions based on the family’s risk tolerance, long-term goals, and market trends. On the distribution side, a family relative, friend, or close family confidant who knows the family well can direct the trustee on all distribution decisions.

The true benefit of a directed trust lies in its ability to leverage specialized expertise as well as giving the family a modicum of control over investment and distribution decisions while ensuring compliance with the trust’s objectives and the beneficiaries’ needs. In the directed trust model, the fiduciary risk transfers from the trustee to the investment and distribution advisors making decisions related to the trust.

Discretionary Trusts: Empowering Trustee Autonomy

In contrast, a discretionary trust structure endows the trustee with broader decision-making authority regarding investment strategies, asset allocation, and distribution decisions without requiring a designated advisor dictating specific actions.

Consider a scenario where a trustee, possessing financial acumen or engaging professional advisors, manages the trust’s affairs autonomously. This trustee navigates diverse investment landscapes, balances risk and reward, and executes decisions aligned with the trust’s objectives and beneficiaries’ best interests.

While providing trustees with substantial autonomy, discretionary trusts require a profound understanding of financial markets, prudent decision-making, and a comprehensive grasp of the trust’s goals to maximize benefits and mitigate risks effectively. From a fiduciary risk perspective, a discretionary trustee is fully liable for all aspects of the trust administration.

Selecting the Appropriate Trust Structure: Factors and Considerations

The choice between directed and discretionary trusts hinges on several critical factors:

• Access to knowledgeable advisors

For a directed trust to work as intended, the grantor/settlor must have individuals or committees of individuals that are knowledgeable on the investment and distribution of trust assets. Because these roles carry significant fiduciary risk, having access to competent advisors is critical. Often the settlor/grantor will name family members or friends into these roles so that they can assert and maintain a level of control. While naming a friend or family member may sound like a good idea, it can lead to serious issues. A friend or family member can be trust-worthy in all aspects, but they may lack the legal, tax, accounting, or investment knowledge necessary to effectively manage the trust’s assets and liabilities. This lack of knowledge and experience can expose the trust to significant risk and is often the basis of long and costly trust litigation. E&O insurance is unavailable to trust advisors, so in the event of a bad outcome, the trust may be left with no recourse or remedy. Unfortunately, friends or family members will not have insurance to cover them in their capacity as advisor, resulting in exposure to unnecessary risk or even legacy-ending losses to the trust.

• Situs Considerations

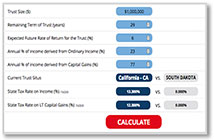

Moving trusts from high income tax states to no tax states like SD, DE, NV, or AK often makes sense for HNW and UHNW families who benefit from the tax savings, asset protection, and privacy these states provide. Since moving assets from these high tax states erodes the tax base of the state, some states have tried to stop this flow by tightening their tax and trust laws. For example, in California – which has the highest state tax rate in the country – if you have a trust that is sitused outside of California, but you have a California resident acting in a fiduciary role such as a co-trustee, investment advisor, distribution advisor or protector, the trust becomes subject to CA tax. For families looking to escape the CA tax web, using a discretionary structure makes the most sense since the fiduciary is out of state and shielded from the reach of CA. Having advisors and protectors that are non-CA residents will optimize the tax structure for a California family looking to set up a directed trust.

• Trust Asset Liquidity

One of the primary uses of trusts is to minimize estate tax. This works particularly well for assets that may dramatically increase in value. One example of this is a founder’s equity in high-growth startup companies or stocks and options given to employees of these companies. Because these assets are illiquid and may sit in trust for 5-10 years before a liquidity event, setting up a directed trust makes sense. The fees are lower than in a discretionary trust, and the grantor will likely want to minimize fees until they have a liquidity event. Founders who don’t have much investment, legal, or tax experience may want to move to a discretionary trust model after the liquidity event. The trust may now have a large concentrated stock position representing a substantial net worth of the founder, and they need a trustee with experience dealing with these situations to protect the founder’s legacy.

• Settlor Preferences

Understanding the settlor’s desires and intentions for the trust helps in aligning the structure with their vision and objectives. For many people setting up a trust, the concept of turning over the title to assets in a trust to a third party is a difficult concept to understand, especially from a control perspective. In these situations, it makes sense to use a directed model if they have experienced advisors that the grantor trusts in those roles. On the other hand, a settlor/grantor may prefer turning the assets over to an independent that will be purely objective when it comes to distribution decisions to avoid family strife between siblings or other relatives that are often named as trustee. In this situation, using a discretionary trust model might work best.

Understanding the intricacies of directed and discretionary trusts empowers advisors and attorneys to tailor solutions aligned with the unique circumstances and objectives of their clients.

Sterling Trustees prioritizes informed decision-making in trust management. Our mission is to provide comprehensive guidance, empowering you to navigate the complexities of trust structures and safeguard and grow your clients’ wealth effectively. If you have any questions or would like to learn more about directed and discretionary trusts and how they can benefit your clients, please contact us to schedule an introductory discussion.

Download this article

Let’s talk. Schedule a date and time to talk about the benefits to your practice of working with an independent corporate trustee.