Trusts 101: Perfect Storm – the Looming Threat to Your Investment Advisory Practice

A perfect storm is a critical situation caused by a “powerful concurrence of factors.”

In our view, there’s a perfect storm on the horizon threatening to disrupt the way the investment community must relate to their own clients. We present three component threats below that comprise a looming threat to businesses working in this community.

Threat #1: The Great Wealth Transfer

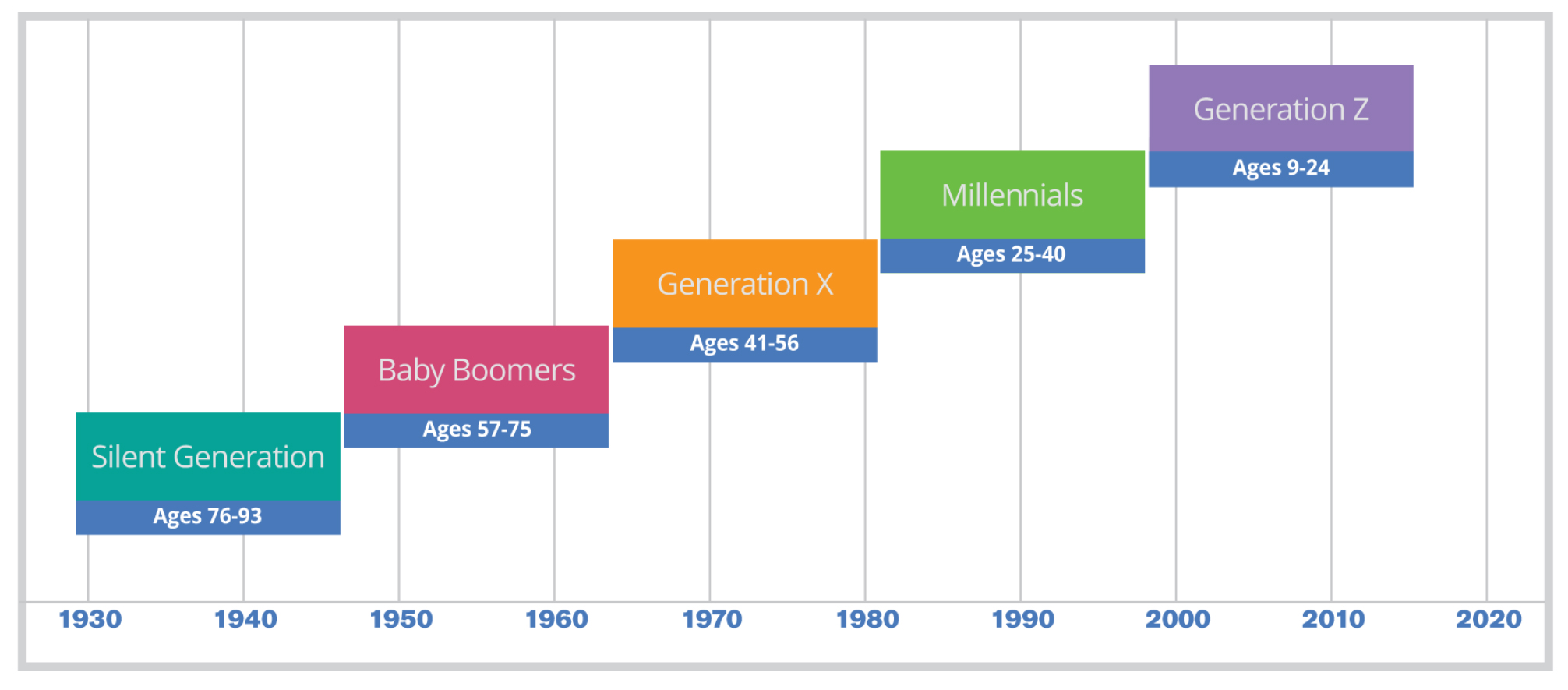

By the end of 2020, Baby Boomers held nearly $60 trillion dollars in US wealth (approximately 53% of total US wealth), followed by Generation X with just under $29 trillion (roughly 25%) with Millennials controlling just over $5 trillion (about 5%) of US wealth.

Over the next 20-25 years, the “great wealth transfer” is expected to shift nearly $70 trillion dollars from Baby Boomers to their Generation X and Millennial heirs. What does this shift mean for your AUM?

What’s the potential impact to you? Who are your clients? What portion of your assets under management are held by members of the Baby Boomer generation?

What’s the potential impact to you? Who are your clients? What portion of your assets under management are held by members of the Baby Boomer generation?

Threat #2: “Shirtsleeves to Shirtsleeves in Three Generations”

Research has shown that nearly 70% of families lose their accumulated wealth in the second generation, while 90% lose it in the third.

Common misconceptions about inherited wealth include the expectation that high net worth parents discuss their wealth and provide guidance to their children about how to manage the family money, and that individuals who come from family money are financially literate.

In reality, almost 80% of HNW individuals lack confidence that the next generation is capable of responsibly handling their inheritance, and nearly 65% have disclosed almost nothing to their children about their wealth.

Perhaps more troubling is the research suggesting that when people inherit considerable wealth, 70% to 90% of them quickly fire the financial advisor on whom their benefactor relied.

Does this accurately describe your clients? Can you help take an active role to address this? What connects you to your clients, and their heirs, moving forward?

Threat #3: The Millennial Paradigm Shift

Millennials have had access to an array of technology tools since birth, so it is not surprising that they are inclined to rely on these tools to meet their needs, including their wealth management needs. Apps and social media are replacing quarterly reports and in-person engagement with financial advisors. News stories have noted for years that nearly 75% of Millennials would prefer to text, rather than talk with other people.

A CNBC story focused on generational views about financial advice, investing, and retirement, indicated that Millennials are twice as likely as the younger members of the Baby Boomer cohort to consider using a robo-advisor for investment needs. Nearly 60% of Millennials believe that financial advisors are motivated by the desire to make money for themselves and their employers, rather than their clients.

Many businesses working with investors are looking closely at their current technologies and how well-positioned they are to support this emerging trend. Do you have the tools that you need to engage with, and retain, the next generation?

What Can You Do Now to “Weather the Storm”?

The preservation of your current AUM, and a connection to the heirs of your high net worth clients cannot be assumed. Complacency is not your friend. How much of your business is at risk in the next five years? Ten years?

One easily attainable approach to helping protect your clients’ wealth, and “lock” in your AUM with a long-term strategy is through the use of trusts.

How do trusts help to manage the risk?

Trusts offer control, flexibility, and protection for assets, and the preservation of AUM. Recognized benefits include safeguarding of assets from bankruptcy, business decline, and civil litigation.

Trusts also offer the opportunity to direct how and when assets are invested and disbursed, preserving them even if beneficiaries are young, inexperienced, or lack the ability or interest to manage increased wealth. With the use of directed trusts, you as the advisor can actually be written into the trust document as the investment advisor going forward ensuring your position even after your client has passed away.

As changing definitions of family and relationships become increasingly more widespread, a trust provides the ability to select beneficiaries that, unlike a will, is not readily subject to challenge. Still other advantages include privacy and tax benefits.

The best way to leverage the advantages of trusts is to work with a knowledgeable partner who is both experienced at managing the trust details as well as independent from investment strategy guidance — a very important point.

An experienced independent corporate trustee is neutral and objective. Not motivated by commissions or outside influences, these trustees avoid any conflict of interest in the handling of assets and distributions. Independent corporate trustees understand the relevant legal requirements and tax implications and have experience dealing with any issues that may arise.

Trusts offer investment advisors the ability to both protect your existing business (AUM) as well as help grow your business.

For example, industry experience shows that you have an 80% chance of retaining the AUM of a deceased client if the assets are in a trust, and only a 20% chance of retaining the AUM if the assets are not in a trust.

In our next post, we’ll take a closer look at how trusts can help you protect your AUM.

Download this article

Let’s talk. Schedule a date and time to talk about the benefits to your practice of working with an independent corporate trustee.