Trusts 101 for Investment Advisors: Types of Trusts Explained

Are you advising your clients on the transfer of wealth through generations via a trust?

Trusts are a powerful vehicle to ensure the continued safety of your clients’ assets while adding to your book of business. However, laws and regulations around trusts are complex and differ across states. As an investment advisor, understanding the variety of trusts and different ways they can be administered will benefit your client and build loyalty for you and your firm.

South Dakota offers some of the country’s most progressive trust laws, allowing you to situs trusts for your clients – leveraging advanced asset protection, perpetuity, privacy and tax laws.

As an independent South Dakota-chartered trust administration company, Sterling Trustees regularly consults with investment advisors on specific trusts that may be helpful planning tools.

Common Methods of Trust Administration

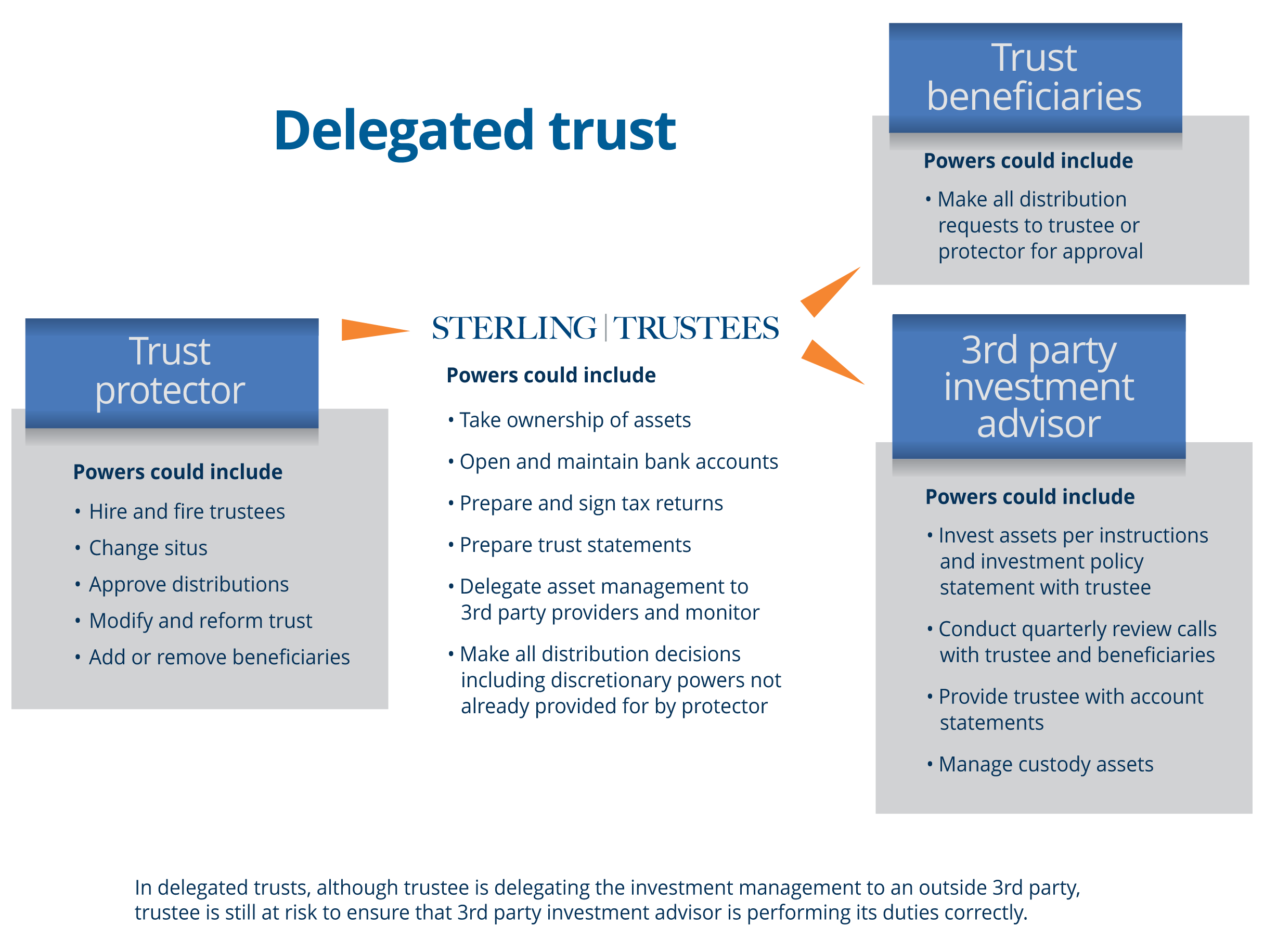

Before going into specific types of trusts, it is important to understand two commonly used trust administration methods and their fiduciary risks. Below we examine discretionary trusts, also known as delegated trusts, and directed trusts.

Discretionary Trusts

The discretionary trust names a trustee who delegates investment management to one or more investment advisors according to a trust document or external agreement. The trustee is then responsible for monitoring performance of each appointed investment advisor. At any time, the trustee can remove investment advisors and appoint someone else if they fail to perform.

The trustee likewise controls distribution decisions and typical administrative functions. As an added layer of protection, a discretionary trust may also appoint a protector – a super fiduciary, who can hire and fire trustee at will. Some protectors have other powers, for instance, making decisions side by side with trustees regarding distributions and investments.

It is worth noting administrative fees for discretionary trusts tend to be higher than directed trusts due to higher fiduciary risk associated with oversight of investment portfolio and distribution decisions.

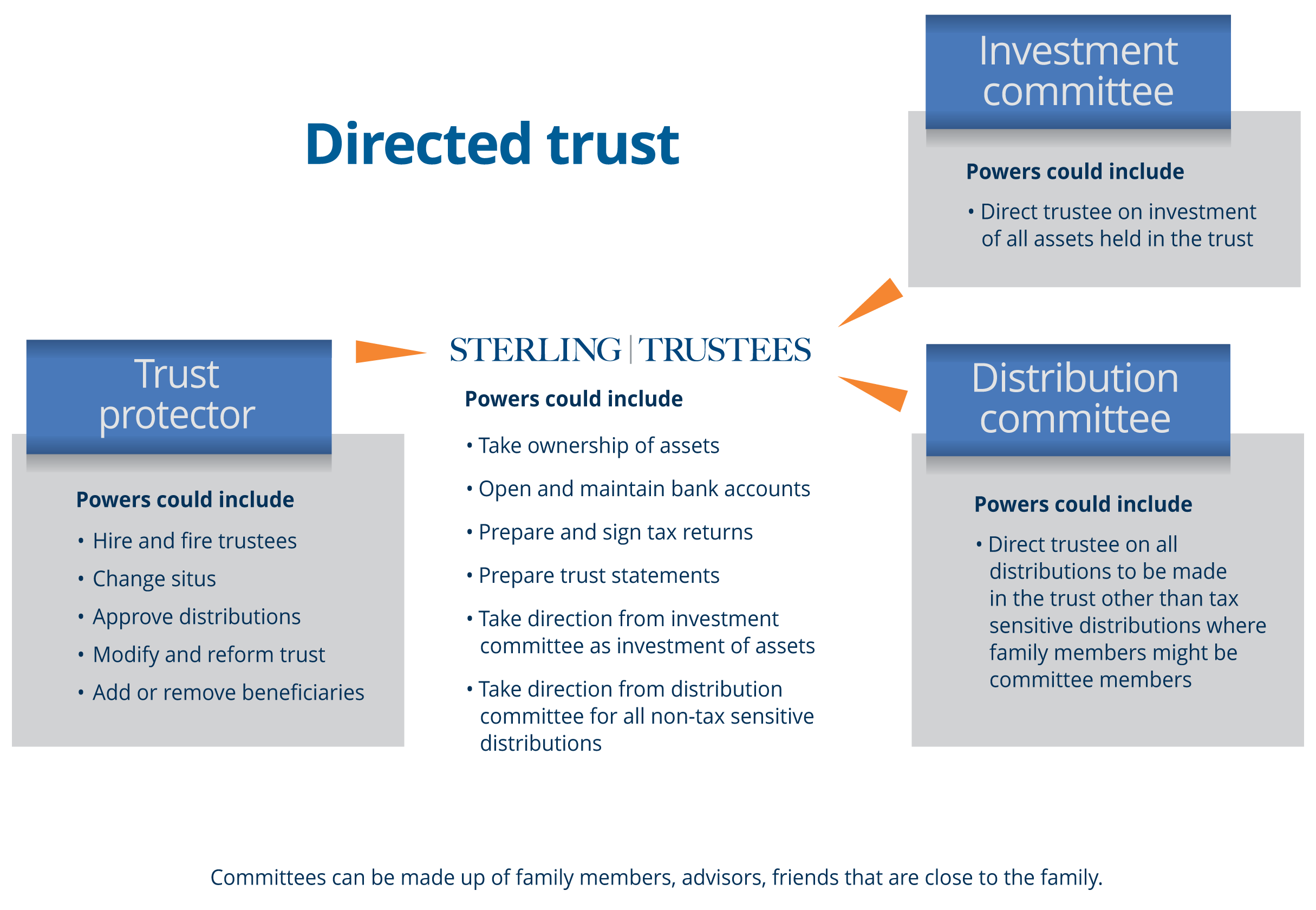

Directed Trusts

The directed trust offers greater versatility and control for families while limiting risk to trustees. Here, the trustee is directed as to all distribution and investment decisions, relieving the trustee of fiduciary risk inherent in a discretionary trust.

Typically, four parties are involved in this fiduciary arrangement. Along with trust administrators, three stakeholder groups may include family, friends or advisors, as chosen by the grantor (person putting money into the trust). These groups perform various functions:

- Trust protector – makes important decisions regarding the trust, i.e., hiring and firing trustees, changing situs, adding or eliminating beneficiaries, approving distributions and modifying or revising the trust.

- Distribution advisor/committee – instructs trustees on all distributions to beneficiaries, excluding those that are tax-sensitive, and presents a letter of direction to the trustees outlining how distributions are to take place. This power can rest on one person or a committee.

- Investment advisor/committee – appoints relevant parties responsible for managing the investment of trust assets. The advisor or committee along with the appointed investment manager then directs the administrative trustee on matters of investment and generally acts according to an Investment policy statement.

- Trust administrator – appointed by grantor or protector. The trust administrator performs administrative trustee duties, including opening and maintaining bank accounts, taking ownership of assets, preparing tax returns and taking direction from distribution and investment advisors/committees.

Choosing the Best Administration Model

Clients generally decide between a discretionary or directed trust based on personal preference and family dynamics.

Some families prefer a discretionary trust. All investment and distribution decisions are controlled by the trustee, who is independent and removes family dynamics and bias from administration. For others, greater direct control over assets leads to the directed trust, moving risk to the investment advisor and distribution advisor. Any trust can be managed on a discretionary or directed basis, including both revocable and irrevocable trusts.

By setting up this type of trust administration in South Dakota, your clients enjoy additional benefits. For instance, South Dakota’s trust-friendly and hospitable tax environment is used in combination with other factors, such as the ability to retain preferred advisors, to ensure optimal outcomes.

Different Types of Trusts

While the basic elements and structure of trusts remain consistent, different types of trusts hold distinct advantages, depending on a family’s asset protection requirements. Knowing differences between trusts can help you make smarter decisions for your clients.

There are two distinctive trusts – the Self-Settled Trust and the Dynasty Trust – which provide unique benefits only available in a handful of U.S. states, including South Dakota.

Self-Settled Trusts

A self-settled trust is generally an irrevocable trust, which allows the grantor to be a trust beneficiary as long as an independent trustee is appointed to make all distribution decisions.

Self-settled trusts provide many other benefits, including building wealth outside of a grantor’s taxable estate, multi-generational planning and protecting family wealth from potential future creditors. South Dakota is one of only 17 states to allow this more complex type of trust.

Self-settled trusts offer asset protection from future creditors or lawsuits. Provided the trust does not contain any ascertainable distribution standard or mandatory distribution of income or principal, it can prevent future creditors from accessing trust assets. Therefore, assets are wholly protected, provided the grantor is not subject to any creditor claims when establishing the trust. Due to its benefits, this trust appeals to those with professions that put them at high risk of lawsuits.

Another significant benefit is reducing transfer tax liability by taking advantage of the lifetime gift tax exemption. The grantor can transfer low-basis assets with high growth opportunities into this trust to minimize estate tax liability. For example, it is advantageous for an entrepreneur with founder shares in a company that has high growth opportunity. The increase in value is transferred to the trust and out of the owner’s estate.

Note that law requires the grantor to appoint a trustee domiciled in the proposed trust situs state. In addition, the grantor has no control over distribution decisions made and carried out by the independent trustee.

Dynasty Trusts

A dynasty trust is a long-term trust. It is created to pass wealth from one generation to the next without incurring transfer taxes – such as estate, gift or generation-skipping transfer tax (GSTT), for as long as assets remain in the trust.

Duration is this trust’s most prominent feature. In the past, trusts were only allowed to remain in place for a specified period of time. Various states have a rule against perpetuities, which dictates when trusts are to terminate. Often, the rule dictates the trust can only remain active for 21 years after the passing of the last beneficiary alive when the trust is created.

South Dakota was the first state to abolish the rule against perpetuities. As a result, properly funded trusts can last forever. Since assets remain in the trust and are not transferred from one generation to the next, the trust is never subject to generation-skipping tax. While dynasty trusts do incur tax on capital gains and income at the federal level in many states, including South Dakota, it is not subject to state income or capital gains taxes.

Additional Types of Trusts

Numerous other types of trusts exist to serve your clients’ specific needs:

- Spendthrift Trust – established for an individual unable to curb personal spending. An independent trustee makes decisions regarding how beneficiaries use money or assets.

- Qualified Terminable Interest Property Trust (QTIP) – allows the grantor to leave assets for a surviving spouse and dictate how remaining assets are then distributed following the spouse’s death. QTIP trusts come in handy when beneficiaries from a previous marriage exist, but the grantor dies before the spouse or partner.

- Grantor Retained Annuity Trust (GRAT) – the grantor can contribute assets to this trust, maintaining a right to receive the original asset value while earning the 7520 rate, also known as the AFR rate as specified by the IRS over the GRAT’s set term. On expiry of the term, leftover assets (after taking appreciation and IRS-assumed return rate into account) are transferred to the grantor’s beneficiaries. Through a GRAT, the grantor can potentially hand over a significant amount of wealth to the next generation at a minimal or even zero cost for gift tax.

- Irrevocable Life Insurance Trust (ILIT) – owns and controls a term or permanent life insurance policy (or policies) while the insured is alive. It also manages and distributes proceeds paid out upon the insured’s death. Conventionally, this type of trust saves assets for specific purposes, such as to pay estate taxes, because the assets themselves are not taxable. ILITs are irrevocable living trusts that cannot be revoked.

- Special Needs – a type of trust that allows a physically or mentally disabled or chronically ill person to receive income without reducing their eligibility for the public assistance disability benefits provided by Social Security, Supplemental Security Income, Medicare or Medicaid.

Get Assistance with Your Trusts

Savvy investment firms have benefited from forging a solid alliance with an advisor-friendly trust administration company that understands their unique challenges.

At Sterling Trustees, we collaborate with prominent investment advisors to safeguard their business and clients’ interests. Our team helps ensure that a family’s legacy continues under their advisor’s watchful eye while growing the investment firm’s client roster as assets pass to the next generation.