Trusts 101 For Investment Advisors: What Is a Trust and How Do Trusts Work?

As baby boomers have started reaching retirement age, the next 30-40 years will see the largest ever transfer of wealth between generations. For investment advisors, this creates a huge opportunity not only to gather new assets but also make sure that you don’t lose any existing clients assets.

One opportunity that investment advisors often overlook, or don’t take advantage of, is discussing trusts with their clients. Trusts can be a vehicle to protect a client’s assets for the next generation, while simultaneously helping an advisor protect his/her own current book of business.

Many investment advisors might not be aware that if their clients’ existing assets are already in trust, the chances of that investment advisor holding onto those assets for the next generation is approximately 80%. However, if those assets are not in trust, that number drops to approximately 20%.

So, if you would like to protect your book of business, as well as help your clients protect their assets as they pass to the next generation, it is imperative that they are knowledgeable about trusts, how they work, why to use them and where to host (situs) a trust. These are just a few of the questions we will try to answer here.

What is a trust?

A trust is a fiduciary relationship in which one party, known as a grantor or settlor, gives another party, the trustee, the right to hold title to property or assets for the benefit of a third party, the beneficiary. Trusts are established to provide legal protection for the trustor’s assets, to make sure those assets are distributed according to the wishes of the grantor/settlor. Trusts are often associated with high net worth families, although anyone wishing to protect privacy, save time, and preserve wealth through multiple generations can take advantage of a trust.

The trust document lays out the grantor’s wishes regarding how trust assets are to be managed and distributed. Typically, distribution of assets is based on some sort of standard such as the health, education, maintenance, and support of the beneficiary or it could be formulaic in that, for example, the net income of the trust can be passed out each year.

What roles are involved?

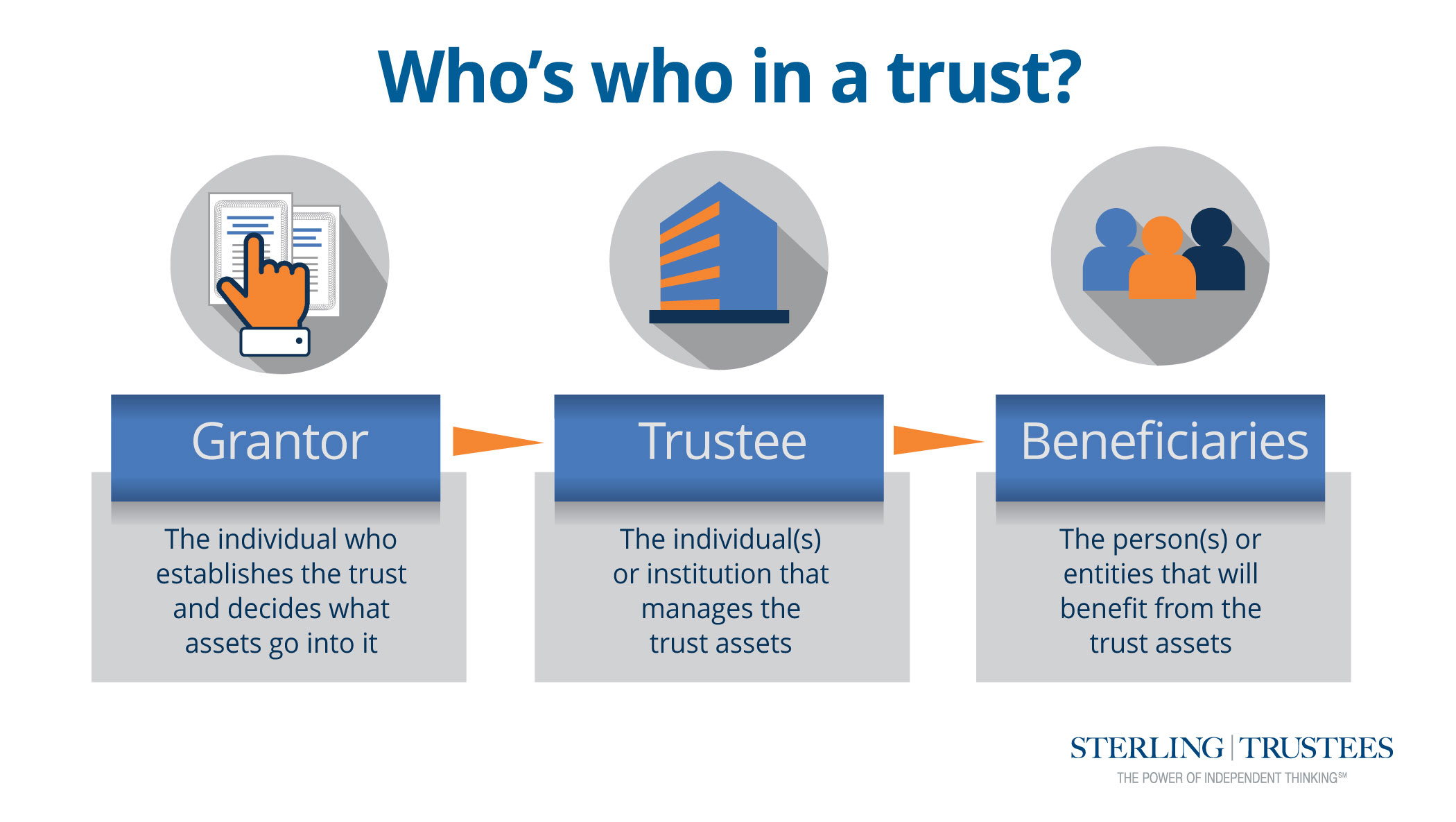

The basic players in the modern arrangement are:

- The Grantor

Also known as a trustor or settlor, this individual establishes the trust and determines which assets go into it. - The Trustee

An individual or institution holding and managing trust assets for the benefit of the beneficiary. - The Beneficiary

The person, people, or entities benefitting from the trust assets.

How do trusts work?

How do trusts work?

Trusts begin with an individual wishing to protect and pass on his or her assets – the grantor. The grantor appoints a trustee as trust administrator to hold the assets according to terms set out by the grantor.

The trustee holds the assets and follows the terms of the trust as set out by the grantor to ensure beneficiaries receive their due under the arrangement. Trustees also act as intermediaries between the beneficiaries and grantor to ensure assets are preserved and conflicts are resolved.

Beneficiaries gain access to the trust and assets through the appointed trustee.

Trusts can be arranged in many ways. The terms set by the grantor will dictate exactly when and how the trust assets pass on to the beneficiaries.

Categories of Trusts

Although there are many different types of trusts, each fits into one or more of the following categories:

- Living or Testamentary

A living trust – also called an inter-vivos trust – is a written document in which an individual’s assets are provided as a trust for the individual’s use and benefit during his lifetime. These assets are transferred to his beneficiaries at the time of the individual’s death. The individual has a successor trustee who is in charge of transferring the assets. A testamentary trust, also called a will trust, specifies how the assets of an individual are designated after the individual’s death. - Revocable or Irrevocable

A revocable trust can be changed or terminated by the grantor during his lifetime. An irrevocable trust, as the name implies, is one the grantor cannot change once it’s established, or one that becomes irrevocable upon his death.

Living trusts can be revocable or irrevocable. Testamentary trusts can only be irrevocable. An irrevocable trust is usually more desirable. The fact that it is unalterable, containing assets that have been permanently moved out of the grantor’s possession, is what allows estate taxes to be minimized or avoided altogether.

Why use a trust?

Trusts can be used for many purposes other than as a tool for moving assets from one generation to another. Some of these purposes include:

- Asset Protection

Provisions can be made in a trust to protect assets from creditors, reducing the risks posed by unexpected lawsuits, divorce settlements, and protecting children from gaining access until responsible enough to handle wealth-related issues, as well as other unforeseen misfortunes. South Dakota’s self-settled trust statutes, for example, allows an individual to set up a trust for his or her own benefit (i.e., the grantor can also be a beneficiary) as long as an independent third party makes all the distribution decisions. If this condition is met, the assets are creditor protected. - Preserving Privacy

Trusts are private. South Dakota does not require the trust to be filed in the public record, unlike a will. - Avoiding Probate

Probate is the transfer process by which assets in a will are retitled from a deceased person to the named beneficiaries. The process can be lengthy, costly, and in the public eye. Probate can be avoided by placing assets in a trust, which administers benefits to the beneficiaries with no interruption or public scrutiny. - Asset Management

Unlike a will, a trust allows an investment advisor or trustee to manage a client’s assets and achieve continuity in the management, eliminating the need to find a new investment advisor, asset manager, or custodian when the grantor passes on. Transfer to the trust is automatic, and asset management is continuous. - Capacity Planning

If the grantor or trust beneficiaries become incapacitated or disabled, trusts protect court-ordered guardianship or conservatorship of the assets. The trustee can continue administering and managing the assets according to the set terms laid out in the trust document. - Dependent Support

Trusts allow funds to be distributed to minors or adults who may be ill equipped to handle money due to age or other factors such as health issues. In such a case, the trust allows for the provision of funds to beneficiaries with special needs who might otherwise be subject to government divestment if assets were out of trust.

Where should you situs the trust?

Trust law and legislation varies widely across the United States. Each state has its own codified trust law and understanding the differences between what each state’s laws are and how you can take advantage of it is key to helping your clients over the long term.

For example if you are a New York resident and want to set up a trust, the trust does not have to be guided by New York trust law. As a New York resident you can set up a trust in any state in the country to take advantage of the state’s trust law.

South Dakota for instance has some of the most progressive trust laws in the U.S., such as no rule against perpetuities, no trust state income or capital gains tax, and enhanced asset protection and privacy. Importantly, it allows for directed trusts where traditional trustee duties can be bifurcated to allow the trust to be administered collaboratively by several expert advisors instead of one. The benefits of situsing trusts in this jurisdiction include:

- Allows directed trusts where trustee duties can be bifurcated to provide exceptional trust administration services. For example, investment advisors and independent corporate trustees like Sterling Trustees can be appointed to work collaboratively for the benefit of the beneficiaries.

- Superior asset protection through the various trust types allowed, including spendthrift trusts and dynasty trusts.

- No trust state income, capital gains, or generation-skipping tax

- Best privacy laws in the country

- No rule against perpetuities

- Attractive decanting, modification, and reformation statues

How do investment advisors and trust companies work together?

Collaborating with a trust administration company — well, to be fair, the right trust administration company — will not affect your client relationship or account.

The right trust administration company operates as a partner to investment advisors, focusing solely on trust administration and separating that service from offering any investment management services. This unbundling of services lets the advisor provide financial advice while the trust company independently administers the trust process, resulting in happier clients, less risk for the clients’ next generation and eliminating all conflicts of interest. With this approach, investment advisors seamlessly maintain client accounts across generations by using an independent trust administration firm

Sterling Trustees is a leading example of this type of partner trust company for investment advisors. Working with Sterling’s approach, investment advisors always retain complete control over their client accounts, which stays on their platform as they guide the client experience.

In addition, Sterling helps investment advisors and their clients take advantage of the benefits from South Dakota as situs, which leads to continued generational wealth through a reduction in tax and better protection of assets.

How can I learn more?

High net worth individuals and families rely on their investment advisors for solutions to preserve and protect generational wealth for years to come. Sterling Trustees is an “advisor-friendly” partner that is well positioned to support this goal and help advisors and their clients benefit from trusts, without interfering in the essential advisor-client relationship.

If you have questions about the potential of trusts for your clients, please schedule an appointment with us. We’re happy to help answer questions and provide guidance on how trusts can benefit your clients, and your business.

About Sterling Trustees

Sterling Trustees is a boutique South Dakota chartered trust company managing over $5 billion in AUM across 350 trusts and 150 families. Sterling provides trust and administration services to high net worth and ultra-high net worth families in the United States and around the world. We work closely with attorneys and investment advisors to extend their expertise with us in the role of independent trustee. Please visit SterlingTrustees.com for more information.